A Quick Introduction To Investments For Young Working Adults

As many young working adults slog through their nine-to-six jobs to collect a salary at the end of the month, it’s dispiriting how quickly it can be depleted.

Source: Adobe Stock Images

While most of that money will go into savings, necessities, and bills, several folks may choose to grow their funds by parking them in different investment opportunities instead.

If you’re new to the world of investing but are interested in starting or finding out more, here’s a quick introduction to the various ways of doing so.

You might have to be prepared to cut down on nights out at your favourite hotpot joint or your regular bubble tea orders, but it’ll be worth it in the end.

Investments come with varying risks

Depending on your life phase, personality, and risk profile, you may have the stomach to invest in riskier products that may help grow your money without you doing much – or anything – at all.

Source: Anna Nekrashevich on Pexels

In the investment world, different investment instruments usually have varying levels of risk. In general, they can fall under three categories – high, medium, and low.

High-risk investments, as the name suggests, are characterised by their potential for significant returns and a chance of substantial losses.

On the other hand, medium-risk investments are distinguished by their balance of potential returns and losses, with neither side teetering too far towards either end.

Lastly, low-risk investments are a conservative investor’s dream. While they often have lower returns, they also tend to lose very little if it ever comes to that.

With so many different investments, it’s easy to feel spoilt for choice and maybe a little confused, especially if you’re just getting started.

This article will explore what fellow millennials have picked up over the years and how it’s turning out for them.

1. Making it big with high-risk investments like crypto

Let’s talk about cryptocurrency. Before the collapse of Luna, Chester Low, 30, an event planner who invested in it early, saw his “thousands of dollars grow exponentially”.

To give an idea of how much he profited, the 30-year-old claimed that at one point, he had enough money in Luna to afford a home renovation for his new BTO.

Then, just a few months later, he was contemplating getting a condo instead.

Chester’s not the only one who made a killing with Luna at first — when things were going swimmingly, founder Do Kwon was celebrated for turning many into overnight millionaires.

At Luna’s peak in April 2022, each coin was worth around S$161, with early investors seeing their returns skyrocket by 15,900%

Source: Alesia Kozik on Pexels

But in May 2022, Luna crashed into oblivion, with each coin not even cracking a cent to its name after investors lost confidence in the cryptocurrency.

Having invested heavily in Luna and crypto as a whole, Chester wistfully recalls the day of the huge crash, saying, “I tried to catch the dip, even when it dropped from over a hundred dollars to US$50.”

“But it quickly spiralled out of control, to the point when I knew I’d lost everything. I didn’t even have time to react. If I could turn back time, I would pay more attention to the news and do more research. After recognising there was no way back, I would’ve exited and minimised my losses,” he lamented.

Having reflected on this whole fiasco, another Luna investor, 32-year-old Ryan Leong, a bar owner, had this to say:

“Nothing is too big to fail.”

“Although I’m a firm believer in technology, this loss has taught me to keep diversifying my investments even further. With the volatility, it’s important to stick to a plan so that you can afford your losses if they come,” he mused.

So, if you manage to get out with any profit in hand, consider yourself lucky because when it comes to cryptocurrency, only some come out as a winner.

2. Niche hobbies can turn into medium-risk investments

As they start moving up in their careers, some people may feel empowered to make bolder decisions when investing their hard-earned money.

Feeling like they may have some wiggle room, folks may choose to invest in opportunities with some known risks.

Medium-risk investments like Exchange Traded Funds (ETFs) and unit trusts are common tools being touted online and within investment circles.

But today, we’re going to talk about something rather niche but equally enticing from an investment perspective: Pokémon cards.

Hear us out.

Image courtesy of The Baron

Borne from the same boredom-inducing period of the pandemic, Pokémon cards have seen a resurgence over the past three years, with both the young and young-at-heart getting back into the hobby.

The older ones are in it for the nostalgia, whilst the card game itself has advanced by leaps and bounds since its inception in the 90s.

This combination of factors has led prices for certain cards to shoot up into the hundreds and thousands.

Coupled with the ability to purchase boxes of cards in bulk, some have seen this hobby turn into a rather unexpected investment opportunity.

One of them is Pokémon Trading Card Game (TCG) Master, ‘The Baron’, 31.

He told MS News that he played the Pokémon TCG competitively for a few years and was just collecting the cards as a hobby, so he originally did not see them as an investment.

“I never really sold them in the past, but the market got too hot in recent years, and the prices were too good not to sell,” he explained, adding that he can earn back a whopping 10 to 50 times the original price of a card.

There’s a catch, however: “My return on investment (ROI) is based on cards I bought five to six years ago, so they are not an accurate comparison to now because back then, they were cheaper and demand was not as high.”

Still, it could be worth a shot. While niche hobbies have niche audiences, Pokémon is a huge global brand, so finding suitable buyers won’t be a problem.

Image courtesy of The Baron

As far as investments go, it does require a little elbow grease, some form of passion, loads of resourcefulness, and lots of physical space. But if you can crack the code, you may be set for sizeable and quick returns.

3. Cutting down on costs counts as a no-risk investment

If you’ve read through everything so far and feel that you’re much better off without investing in anything that carries risks, you’re not alone.

Accountant Julian Teh, 34, said people always view investments as putting proverbial eggs into a basket or two. “But reducing your own expenses is also a form of investment.”

Given the current economic climate, Teh has become more mindful of his expenditure. To him, it’s helpful to understand his cash outflow and look for ways to stop overspending.

Source: Adobe Stock Images

“This habit doesn’t have to affect your quality of life. It can be as simple as buying less bubble tea, resisting the temptation to buy branded goods, and eating at coffee shops more often,” he noted.

There are many tools that can help keep track of your expenses, such as DBS NAV Planner. You can also use it to set up a budget that includes saving and spending targets.

According to a DBS research report on inflation, the three key components hitting our wallets are:

- Transportation

- Food

- Housing and utilities

These are also the three key drivers of inflation in Singapore. So, by understanding our individual spend habits, we’ll know which areas we can work on to reduce discretionary spend and enhance our financial situation to manage the uncertainties ahead.

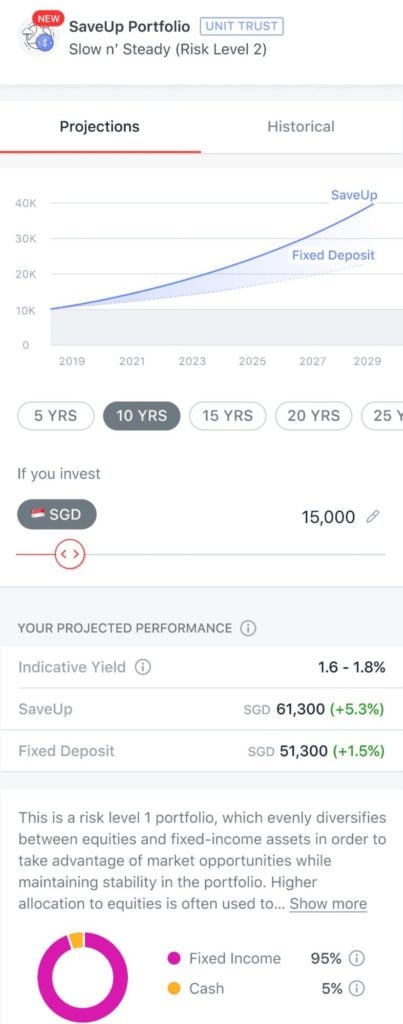

4. Play it safe with ready-made investment portfolios via DBS digiPortfolio

However, if you’re still keen on exploring the world of investing without putting too many eggs into said baskets, there are low-risk but effective options to consider.

Even better if there’s someone or something else doing the investing for you as this helps free up time for you to focus on family, friends, and yourself.

After all, as much as we’d love to maximise the hours in a day, adulting as a young millennial can sap everything out of you. Especially if your daily work schedule is packed with back-to-back meetings and calls.

This is why Shing, 29, recommends the DBS digiPortfolio, a digital platform that helps you optimise investing strategies based on your investment profile. As a busy lawyer who spends most of her day working, she appreciates how easy, hassle-free, and seamless the service is.

Image courtesy of DBS/POSB

Basically, all you have to do is input parameters depending on your needs and goals into your digiPortfolio account. The automated platform will make investment decisions based on trends in the financial markets using a combination of data, artificial intelligence (AI), and human expertise.

In under 15 minutes, users can sign up for an account, verify their identity, and answer some simple questions to help determine their investment profile. After that, just sit back and let the robo-advisor do its job.

And the barrier of entry is extremely low — investors can pump in anywhere between S$100 to S$1,000 to start their journey.

Portfolio managers will also step in to respond appropriately to events and market outlooks if things pick up or dwindle for the worse. They will include commentary explaining these decisions in the portfolio, giving customers added peace of mind.

With the speed of technology, the human touch of a seasoned investor, and the backing of a trusted bank, you can rest assured that your money is safe with digiPortfolio.

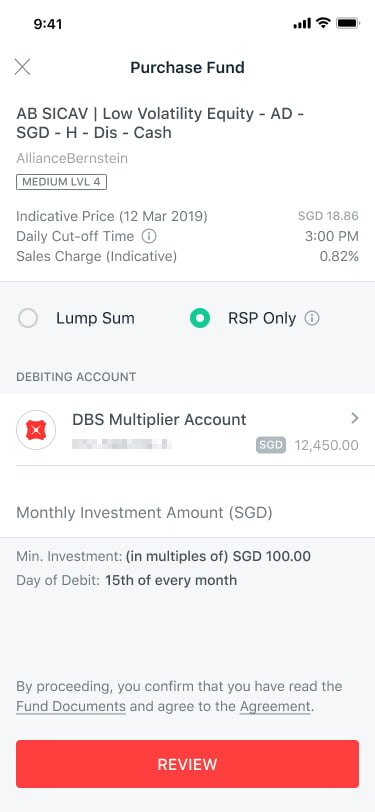

5. POSB Invest-Saver helps you stay consistent

For more of a hands-off approach, new investors can kickstart their journey with POSB Invest-Saver.

Compared to the digiPortfolio, the Invest-Saver requires a one-time setup that repeats the same monthly investments.

Simply allocate a certain amount of cash every month, and the account will automatically invest in either an ETF or Unit Trust of your choice. Through automation, you’ll barely notice a thing as your investments start accumulating steadily and progressively.

Image courtesy of DBS/POSB

This is what Luna Goh, 33, an editor, does: By doing a one-time set-up for POSB Invest-Saver on specified investment instruments, she’s ‘forced’ into investing a percentage of her money every month.

Not that she’s complaining, though — Luna shared that this will help her stop putting off investing or wasting the money on unnecessary purchases.

“It also helps me make use of dollar-cost averaging since I’m putting in something every month,” she added.

Dollar-cost averaging, as DBS explains, involves putting in smaller amounts of money at regular intervals, regardless of the share price.

This is ideal for those who are in the first few years of their career. Although they tend to have less to invest, it still gives them the opportunity to benefit from future market growth.

It can also lower the average cost of investing and help to reduce stress as there’s no need to worry about market timing and other complicated investment strategies.

Last but not least, another huge part of what makes these options low-risk is their flexibility, allowing you to terminate your plan or redeem your holdings at any time.

Young investors have a wealth of knowledge at their fingertips

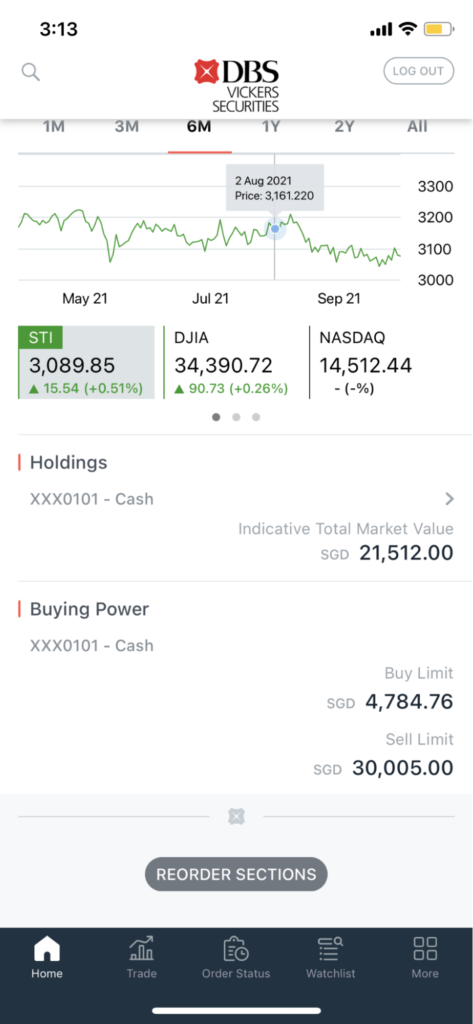

The world of investing isn’t just open to millennials and older — if you’re part of Gen Z, you can start looking into it too with a DBS Vickers Young Investor Account, which is specially designed for those between the ages of 18 and 25.

Image courtesy of DBS/POSB

Do note that customers aged 18 to 20 are required to complete a questionnaire to declare that they possess basic investing knowledge. Those who do not will be directed to the Singapore Exchange (SGX) website.

Once you’ve got your account, download the Vickers app, which gives you access to their online trading platform and advanced investment tools powered by financial technology company TipRanks.

Use it to make trades, stay in the know of current trending stocks, and view analyst forecasts and price targets from experts around the world. All in the palm of your hand.

Image courtesy of DBS/POSB

With flat commission fees and no custody fees for foreign shares, it’s better to jump on the platform quickly to maximise your time with the account.

Plus, if you open a new DBS Vickers online trading account and make a cash upfront trade on the app by 31 Mar, you’ll get S$30 as a reward for achieving this financial milestone.

For more information on investing and other ways to help you be better prepared financially in a time of inflation, visit POSB’s website.

You can also follow the DBS for Young Adults Telegram channel for useful tips on investments and more.

Prepare to live comfortably later by investing early

Well, now that’s a lot of money talk for a day, but if you’ve been thinking about stretching your dollar, this guide might be a good jumping-off point.

After all, everybody wants to live a more secure and comfortable life, and having a little extra cash in the coffers can do just that. Especially if it can grow without you having to put in that much effort — after making the right investment choices, that is.

Disclaimer: This article is not intended to be and does not constitute financial advice or investment advice. Do seek advice from a financial adviser if need be. This ad has not been reviewed by the Monetary Authority of Singapore.

This post was brought to you in collaboration with DBS/POSB.

Featured image by TheSmartLocal.